Frontier & Secondary Markets

Frontier and secondary markets represent the broadest and most varied category of emerging opportunities — ranging from established income streams that are simply underutilized by many landowners, to newer markets still taking shape at the policy and industry level. Some of these, like pine straw, require relatively little infrastructure to enter. Others, like carbon and biodiversity markets, involve longer timelines and more complex participation structures. What they share is that they draw value from the land in ways that complement, rather than compete with, traditional forestry and agricultural uses.

Pine Straw

Pine straw (the fallen needles of pine trees) is a widely used landscaping mulch with consistent regional demand across the Southeast. Landowners with established pine stands, particularly longleaf, loblolly, or slash pine, can rake and bale pine straw as a recurring annual or semi-annual income stream with relatively low startup costs. It is one of the more accessible secondary markets available, and many landowners are already sitting on viable pine straw acreage without realizing it.

Select a topic below to learn about starting and scaling a pine straw enterprise on your land:

At a glance

Pine straw is one of the most accessible non-timber forest products in the Southeast. Landowners with established longleaf, slash, or loblolly pine stands can generate steady annual income starting as early as year 8 – without cutting a single tree.

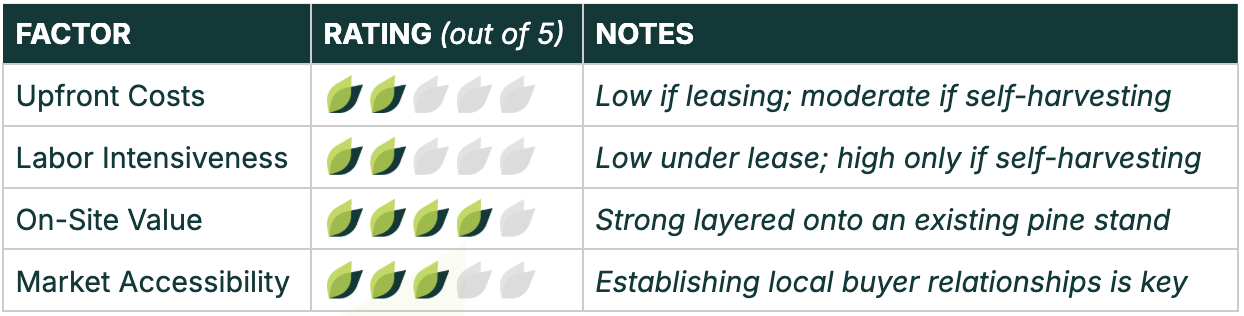

Two paths exist: lease your stand to a licensed contractor (near-zero labor, predictable income) or self-harvest and sell directly (higher revenue, but requires equipment, labor, and market relationships).

Longleaf straw commands the highest market price and is preferred among buyers in the Southeast. A 50-acre stand in good condition can generate $5,000–$12,000+ per year depending on path and stand quality.

Decision Factors

Pine straw works best layered onto an already-established stand. Leasing is the lowest-friction entry point for most small landowners. For those willing to invest in equipment and labor, self-harvesting can yield two to three times the returns of a lease agreement in high-output stands.

Forest Thinning

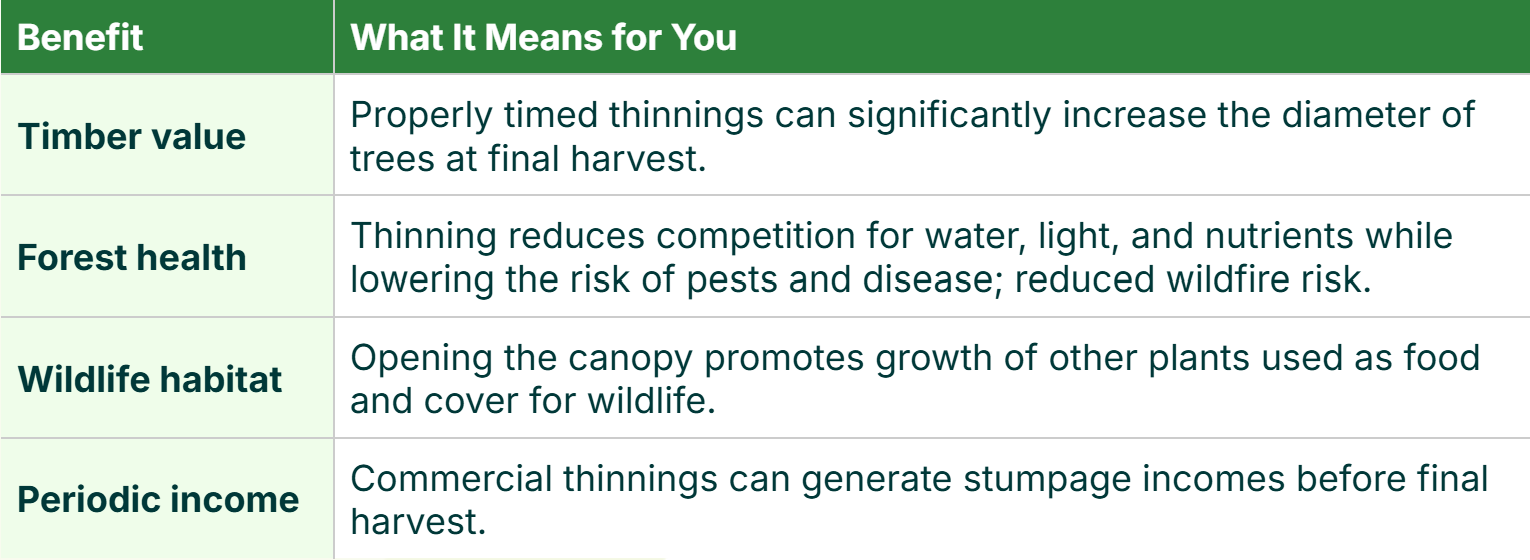

Forest thinning is the deliberate, selective removal of trees from a stand to reduce competition and improve the health, growth, and long-term value of the trees left behind. Rather than clearing land, thinning is a targeted practice, and for most Southeastern landowners, it is one of the most important tools available for managing a productive, healthy forest.

Select a topic below to learn about how to get started when thinking about thinning your forests:

At a glance

There are three primary ways by which forests are thinned:

Mechanized Thinning: Crews using heavy equipment (feller-bunchers, skidders, harvesters) to fell, process, and extract trees. Most common for commercial thinnings with sufficient timber volume.

Manual Thinning: Crews using hand tools like chainsaws or spacing saws without heavy machinery. Common for pre-commercial thinning in younger stands.

Chemical Thinning: Herbicides applied directly to undesirable stems to kill trees without physical removal. Used where no timber market exists or to control hardwood competition in longleaf pine restoration.

Decision Factors

Biochar

Biochar is a carbon-rich material produced by burning woody biomass at high temperatures in a low-oxygen environment — a process called pyrolysis. It has applications as a soil amendment, and growing interest from agricultural and environmental markets has made it an emerging revenue stream for landowners with access to woody material or slash from timber operations. Biochar can also intersect with carbon markets, as its production and soil application represent a form of long-term carbon storage.

Select a topic below to learn about starting and scaling a biochar enterprise on your land:

At a glance

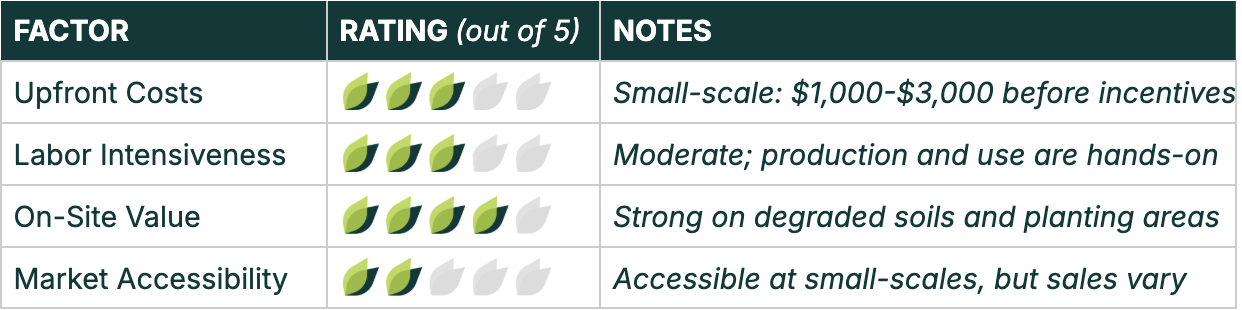

Biochar is a promising, but still emerging forestry practice. For small landowners in the Southeast, the primary use-case is as a soil amendment that reduces input costs.

Federal cost-share through NRCS can help offset startup costs. Note that sign-up is competitive, availability varies by state, and best practices are site-specific.

Small-scale production is accessible for most landowners with existing slash. A realistic entry point is $1,000-$3,000 upfront and 5-10 burn days per year.

Decision Factors

Biochar is most effective when it addresses an existing residue problem through targeted rather than whole-property application. Prospective producers in the Southeast should be prepared for a hands-on process requiring local labor or contractors, as regional demand is still developing.

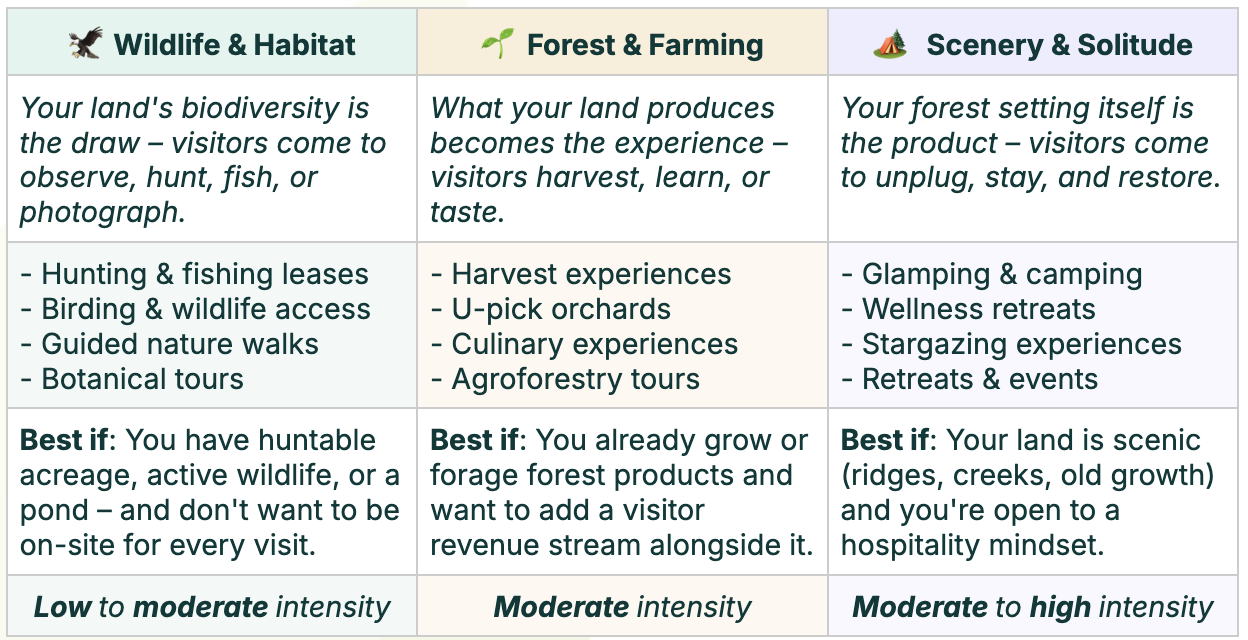

Ecotourism

Ecotourism encompasses a range of fee-based experiences that invite visitors onto working or natural lands — hunting and fishing leases, guided foraging or birding, farm stays, and educational or cultural programming. For landowners with distinctive natural features, wildlife habitat, or cultural history tied to the land, ecotourism can generate income while keeping the land intact and in the family. It requires more direct landowner engagement than most other markets here, but can also be among the most personally meaningful.

Select a topic below to learn about starting and scaling a ecotourism enterprise on your land:

At a glance

There's no one-size-fits-all model. Options range from low-effort (paid hunting access or u-pick harvests) to more involved (guided forest farming tours or glamping), so you can match the approach to your time, budget, and comfort level.

Your forest is already a destination. Ecotourism lets you profit from that without changing what your land fundamentally is.

Small acreage can still qualify. Even 50–200 acres of healthy, accessible forest can support meaningful income from land-based tourism, especially in the Southeast where demand for outdoor recreation and local food experiences is growing fast.

Decision Factors

Recreational leasing is most compelling when your land already offers huntable acreage, harvestable forest products, or scenic features like ridges and creeks, as each of these converts an existing asset into recurring income with minimal additional investment or presence required.

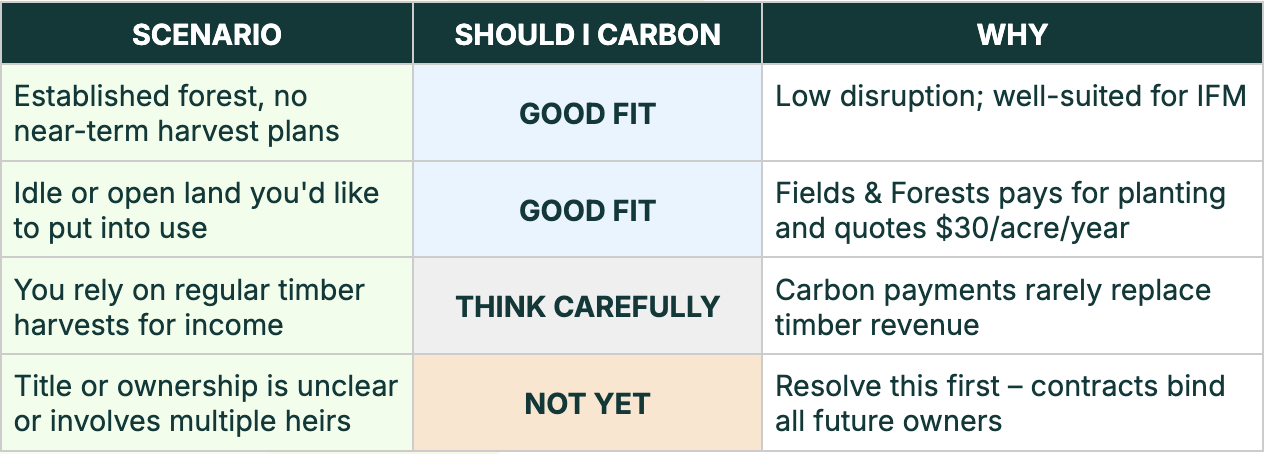

Carbon Markets

Carbon markets allow landowners to generate revenue by demonstrating that their forests are storing carbon that would otherwise be released into the atmosphere. Participation typically involves enrolling in a program through a carbon registry or aggregator, undergoing verification, and receiving credits that are sold to companies or institutions looking to offset their emissions. The market is still evolving — standards, credit prices, and contract terms vary widely — and landowners should approach it with careful due diligence, particularly around long-term land use commitments.

Select a topic below to learn about carbon markets on your land:

At a glance

Carbon markets offer a new income stream from your forest (some strings attached). Programs pay you to keep trees standing and growing, but contracts restrict your land use for 20+ years and bind your heirs.

Small-landowner programs now exist starting at 30 acres. The Southeast is an active region for enrollment, and some programs provide a free forester visit with no obligation to sign.

Expect modest, steady income. Most small-landowner programs pay $10-$30 per acre per year. For a 50-acre tract, that's roughly $500-$1,500 annually.

Decision Factors

Carbon credit programs typically offer guaranteed annual payments and disaster protection over the long term, but work only if your land can demonstrate carbon storage above what would have occurred naturally.

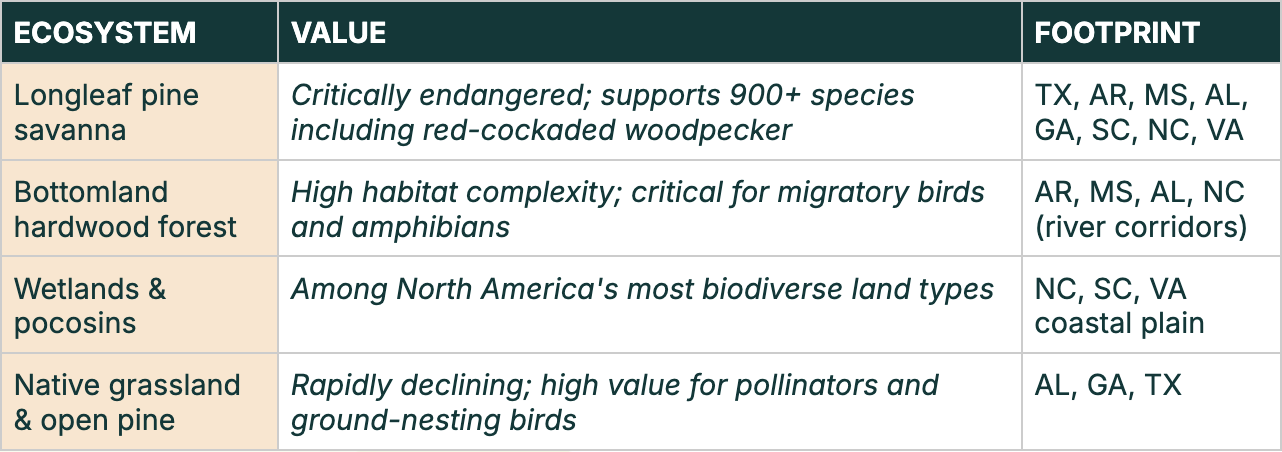

Biodiversity & Habitat Markets

Biodiversity and habitat markets are among the newest and fastest-developing frontier opportunities, driven by growing corporate and regulatory demand for measurable conservation outcomes. Landowners can potentially generate income by restoring, protecting, or managing habitat for specific species or ecosystems — receiving payments through conservation easements, habitat credit programs, or emerging biodiversity credit schemes. This space is still maturing, but landowners with high-quality or restorable habitat may be well-positioned as these markets develop.

Select a topic below to learn about biodiversity and habitat markets on your land:

At a glance

Biodiversity credits pay you for the ecological health of your land, but the US market is still early-stage and not yet reliably accessible for small landowners.

The most accessible habitat payments available today come from USDA programs, not credit markets. That's where to start.

The Southeast is well-positioned for when this market matures. Longleaf pine, bottomland hardwood, and wetland ecosystems are among the most ecologically valuable land types in North America.

Decision Factors

Biodiversity credits lack a universal unit and the U.S. market remains early-stage, but high-priority ecosystems — especially historically rare or ecologically significant types — are most likely to attract buyers.

Remote Landowner Markets

For landowners who live away from their forests – or who may not have the capacity for the labor demands of more traditional forestry markets – making the most of your land can feel out of reach. The markets below are selected for their low barriers to entry, minimal on-site requirements, and income that keeps working whether you're there or not.

Select a topic below to learn about potential markets for landowners who live away from their forests:

Market Directory

The following directory and map are additional resources for landowners looking to double-click into any of the emerging markets covered on this page. The resources listed are not exhaustive, but represent a strong sampling of the information most relevant to small forest landowners in the Southeast. The accompanying interactive map allows landowners to visualize where active market players and providers are located relative to them, helping connect opportunities to physical resources nearby.

| Market | Resource Type | Name | Summary |

|---|---|---|---|

| Pine Straw | Budget | UGA Warnell School of Forestry: Pine Straw Yields and Economic Benefits in Loblolly, Longleaf, and Slash Pine Stands | A University of Georgia economic analysis covering per-acre income ranges, per-bale pricing by species, and rates of return using study sites across Georgia and South Carolina. |

| Pine Straw | Implementation | Alabama Cooperative Extension System: Harvesting Pine Straw for Profit — Questions Landowners Should Ask Themselves | A practical Auburn University Extension guide covering stand suitability, species selection, raking schedules, and equipment options for Southeast landowners. |

| Pine Straw | Market | NC State Extension: Managing Longleaf Pine Straw | An NC State resource covering how landowners sell pine straw, including per-bale and per-acre contracts, sealed bidding, and buyer preferences across the longleaf range. |

| Biochar | Budget | GCB Bioenergy (2025): Biochar Economics for Private Landowners With Payments From Carbon Markets and Federal Incentives | A 2025 peer-reviewed economic analysis focused specifically on private landowners in the southeastern U.S., modeling profitability across manufacturing costs, NRCS EQIP payments, and carbon credit revenues. |

| Biochar | Implementation | American Farmland Trust: Biochar in Agriculture Toolkit | A practical planning resource developed in partnership with USDA NRCS and the U.S. Biochar Initiative, covering production methods, on-farm application, quality standards, and webinars on small-scale biochar production. |

| Biochar | Market | American Biochar Institute: Supplier & Buyer Directory | The leading U.S. biochar industry hub, offering a searchable directory of producers and buyers, quality standards guidance, and market development resources. |

| Biochar | Network | American Biochar Institute: North American Biochar Conference | An annual conference convening 700+ biochar producers, investors, policymakers, and researchers. The 2026 conference is scheduled for November 16–18 in New Orleans, Louisiana. |

| Ecotourism | Budget | USDA NRCS: Agritourism Resource Manual | A comprehensive USDA manual covering financial planning, market demand, business plan development, and federal funding programs available to agritourism operators, informed by 2022 Census of Agriculture data. |

| Ecotourism | Implementation | ATTRA / NCAT: Roots to Revenue — Making Agritourism Work for Your Farm | A practical guide walking farmers through launching an agritourism enterprise, covering liability protection, visitor management, pricing, marketing, and real-world case studies from farms across the country. |

| Ecotourism | Market | NC State Extension / UGA: Agritourism, Your Way | A joint resource from NC State and the University of Georgia's Center for Agribusiness covering market assessment, visitor experience development, business planning, and connecting with regional agritourism networks in the Southeast. |

| Ecotourism | Network | NAFDMA International Agritourism Association | The leading trade association for agritourism operators since 1986, offering peer networking, webinars, an annual convention, and a member directory spanning farm stays, U-pick operations, farm markets, and more. |

| Carbon | Market | UF/IFAS Extension: A Landowner's Introduction to the Forest Carbon Market | A University of Florida extension publication introducing SE landowners to forest carbon markets, covering how credits are generated, the difference between voluntary and compliance markets, and how landowners can participate. |

| Carbon | Implementation | American Forest Foundation & The Nature Conservancy: Family Forest Carbon Program (FFCP) | The leading carbon program designed for small-acreage landowners (30+ acres), offering annual payments, a free forest management plan, and professional forestry support across 20 states including several in the Southeast. |

| Carbon | Implementation | American Forest Foundation: Fields & Forests | A reforestation-focused carbon program exclusively for SE landowners in AL, FL, GA, and SC with 30+ acres of unplanted fields. AFF covers all seedling, site prep, and planting costs, with guaranteed annual payments of $30/acre and full timber harvest rights retained. |

| Carbon | Network | Mississippi State Extension: Voluntary Forest Carbon Markets and Programs for Mississippi Landowners | A practical SE-focused guide covering the types of carbon projects available, how programs are structured, and a list of active developers and programs currently serving small landowners across the Southeast. |

| Biodiversity | Market | Trellis: Biodiversity Credits Are Gaining Traction — A Guide for 2025 | An accessible 2025 overview of the voluntary biodiversity credit market, covering how credits are defined, what drives corporate demand, the key standards bodies, and why the market remains nascent but is accelerating. |

| Biodiversity | Budget | Conservation Finance Network: Species and Habitat Conservation Banking | A practical explainer on the most established U.S. habitat credit mechanism — conservation banking — covering how credits are created and sold, what landowners earn, and how the process works under the Endangered Species Act. |

| Biodiversity | Implementation | U.S. Fish & Wildlife Service: Conservation Banking | The USFWS program through which private landowners can protect and manage habitat for listed species and sell approved credits to developers needing to offset impacts — the most developed and regulated habitat credit market currently operating in the U.S. |

| Biodiversity | Network | USDA NRCS: Wetland Reserve Easements (WRE) | A USDA program paying private SE landowners to restore and protect wetland habitat through conservation easements, with NRCS covering up to 100% of easement value. The most accessible government-backed habitat payment program currently available to small landowners in the Southeast. |